Archives

Feature, Freight News, Logistics, Sea

Market Signals: Freight indexes Point to Early Peak

[ July 3, 2026 // Gary Burrows ]EDITOR’S NOTE: Freight Business Journal North America’s Peak Season Forecast 2026 in the July-August issue brings together leading market analysts and logistics executives to examine whether the current freight rally has staying power, the indicators they are watching most closely, and what shippers should expect during the balance of the year.

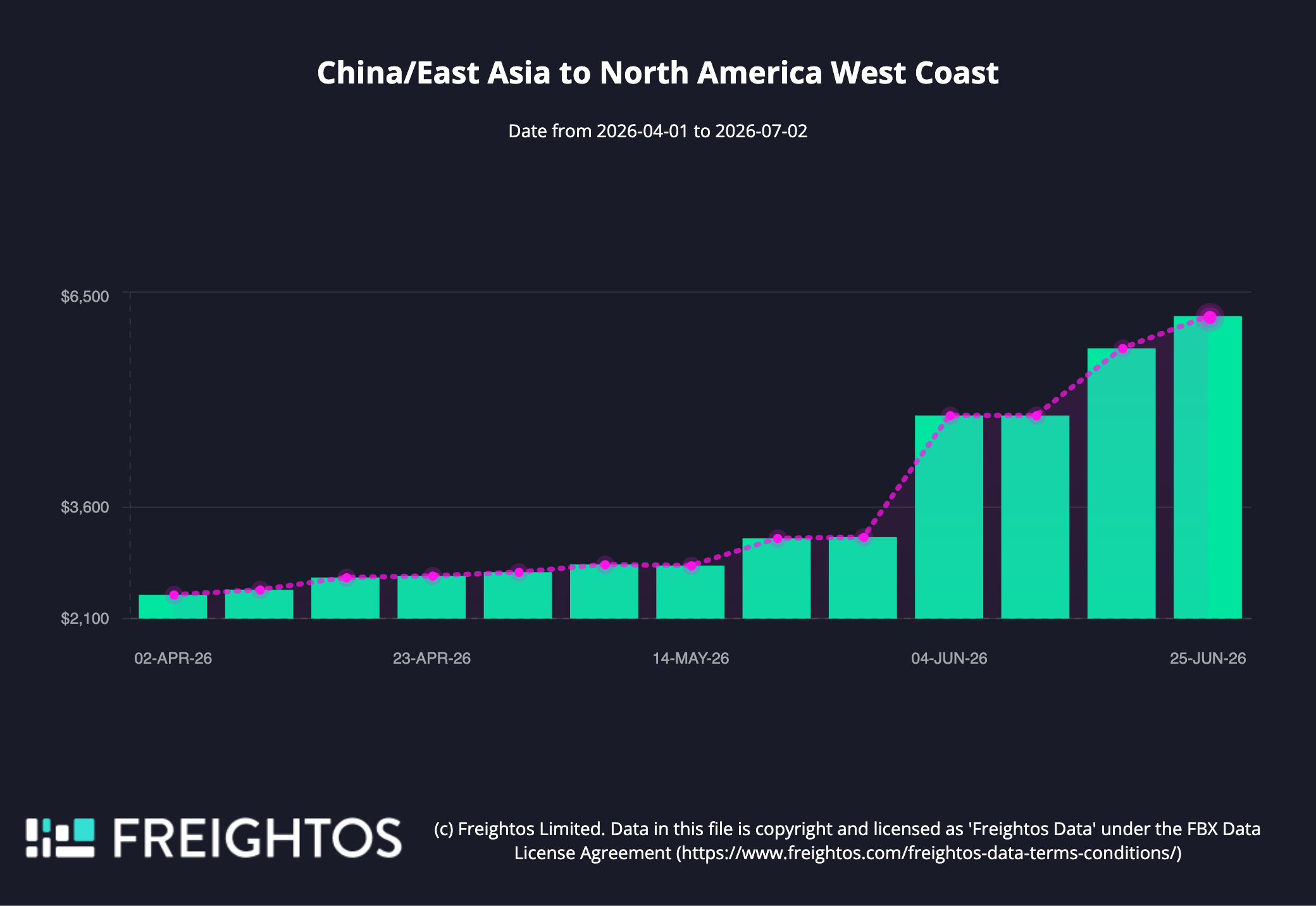

Three of the container shipping industry’s leading market benchmarks are telling the same story: Peak season has arrived early, and strong demand continues to push freight rates higher despite carriers deploying record capacity across the trans-Pacific.

Fresh market updates from Xeneta, Drewry and Freightos show double-digit spot rate increases on key Asia-U.S. trade lanes, reinforcing the view that importers continue to frontload cargo ahead of potential tariff changes and lingering geopolitical uncertainty.

The latest Freightos Baltic Index (FBX) shows spot rates from China and East Asia to the U.S. West Coast climbing sharply since April, while Xeneta reported Far East-U.S. West Coast spot rates reached US$6,639 per FEU as of July 3, up 14 percent from the previous week and 253 percent above pre-Strait of Hormuz crisis levels at the end of February.

“The combination of record capacity deployment and further rate increases on the Transpacific tells us demand is strong and that carriers are scrambling to satisfy it,” said Peter Sand, Xeneta’s chief analyst.

Perhaps the most striking signal is that carriers continue adding ships without slowing the market’s momentum.

Xeneta said offered capacity on the Far East-U.S. West Coast trade reached a record four-week rolling average of approximately 350,000 TEUs, surpassing the previous high established following last year’s 90-day U.S. tariff pause. Carriers including MSC have reinstated services, while Yang Ming and Ocean Network Express (ONE) have introduced additional loader vessels in an effort to accommodate growing demand.

Even so, Xeneta expects spot rates to continue climbing through at least mid-July.

Drewry reached a similar conclusion in its latest World Container Index, which rose 9 percent to US$4,530 per 40-foot container.

Trans-Pacific routes again led the gains, with Shanghai-New York increasing 11 percent to US$7,902 per FEU and Shanghai-Los Angeles rising 10 percent to US$6,349.

Despite additional vessel deployment, Drewry noted carriers have announced eight blank sailings on the trans-Pacific trade for next week, while continuing to implement general rate increases and peak season surcharges. HMM alone announced a US$3,000 peak season surcharge effective July 15.

Drewry expects freight rates to continue increasing over the coming weeks.

The market’s strength appears concentrated on the major east-west trades rather than across all shipping lanes. Drewry’s Intra-Asia Container Index declined for a second consecutive week, suggesting that while regional markets may be stabilizing, long-haul trades linking Asia with North America and Europe remain under significant pressure from early peak season demand.

Taken together, the three market indicators suggest the traditional shipping calendar continues to evolve. Rather than a single late-summer surge, retailers and importers are accelerating shipments amid shifting tariff policies, geopolitical risk and continuing uncertainty over supply chain disruptions.

Whether that momentum can be sustained through the remainder of the year is now the industry’s biggest question.

Tags: Drewry, Freightos, Market Signals, Xeneta