Archives

Feature, Freight News, IT Suppliers, Logistics, People

What July Imports Spike Means for Supply Chain

[ September 5, 2025 // Gary Burrows ]By Jackson Wood

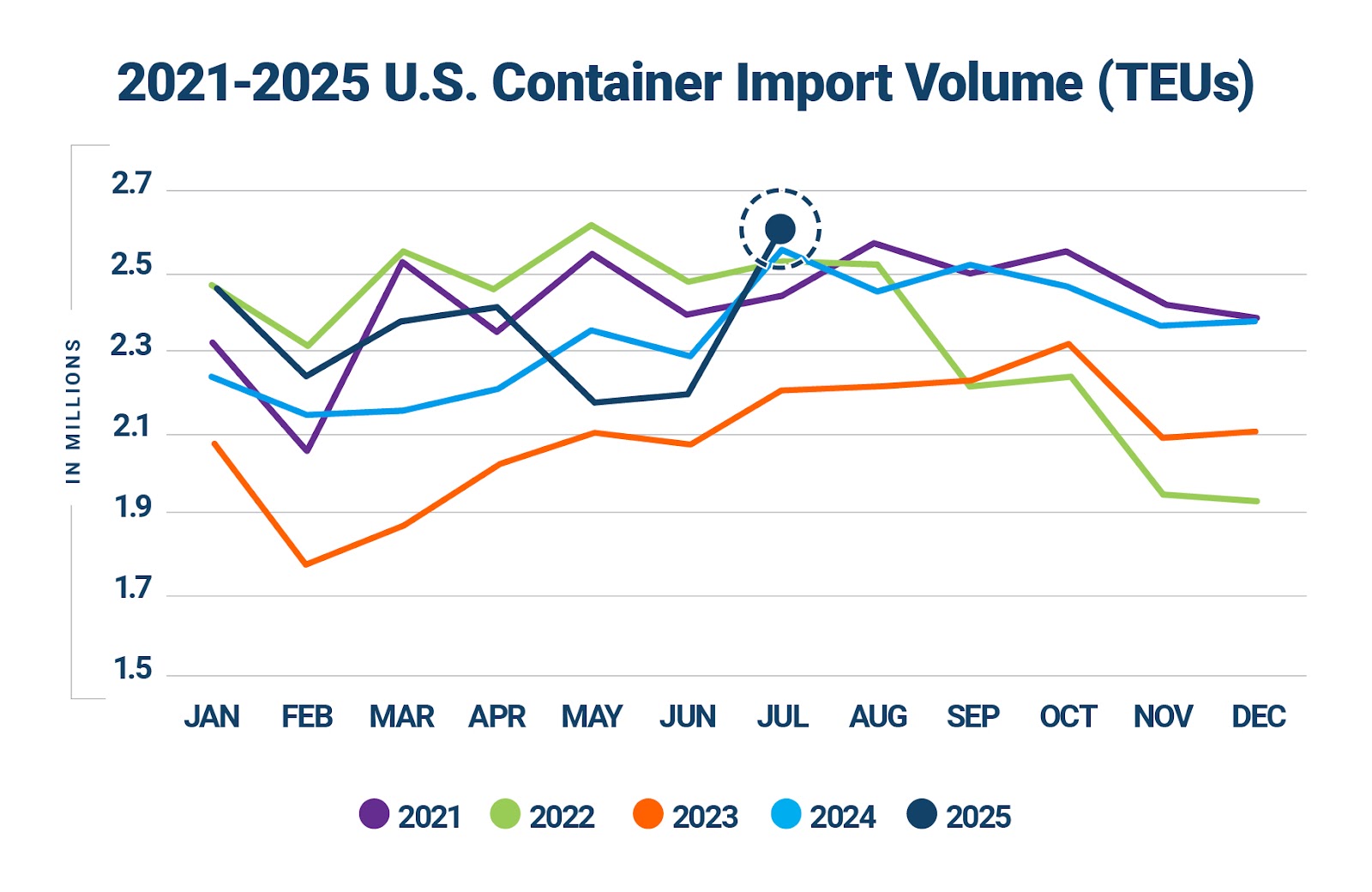

July was a busy month for U.S. containerized imports, following two months of uneven performance. Total volumes surged 18 percent over June to 2.62 million twenty-foot equivalent units (TEU). It’s also a 2.6 percent increase over July 2024 – and just 555 TEUs short of the record set in May 2022.

On the surface, the sharp jump is consistent with seasonal demand as retailers prepare for back-to-school and early holiday shipments. Beneath the numbers, however, lies a more complex story about shifting trade policies and their impact on global supply chains.

Tariff Deadlines Spur Frontloading

One key takeaway from the July U.S. container volume data is that trade policy, not just consumer demand, is increasingly affecting shipping flows and creating uncertainty for global supply chains. To mitigate the impact of tariff changes, importers have been accelerating shipments to bring in inventory in advance of higher rates.

The U.S.-China tariff truce, holding tariffs at 30 percent through Oct. 15, prompted many businesses to frontload orders in the months preceding the end of the agreement – which was extended on Aug. 12 for another 90 days through Nov. 10. In addition, on Aug. 1, the U.S. enacted a broad set of reciprocal tariffs targeting over 60 countries, including the EU, Canada, Japan and South Korea, with rates ranging from 10 percent to 41 percent.

Additional measures include a 50 percent tariff on Indian exports and a universal 50 percent duty on copper. The repeal of the de minimis exemption for all countries follow on Aug. 29, replacing duty-free treatment for parcels under US$800 with flat-rate fees of US$80 to US$200 per item – another disruption for cross-border e-commerce.

China’s Comeback, With Caveats

July also saw a striking month-over-month rebound in U.S. imports from China. This followed a sharp contraction in May and June, when elevated uncertainty with respect to tariffs and the end of the de minimis exemption for China weighed on shipment flows. At 923,075 TEUs, July shipments jumped 44.4 percent from June (649,133 TEUs) and marked the highest monthly total since January (997,909 TEUs). China’s share of U.S. imports rose to 35.2 percent, recovering from June’s 28.8 percent, though still below its February 2022 peak of 41.5 percent.

The recovery demonstrates China’s ongoing dominance in U.S. supply chains, particularly in categories such as furniture and bedding, plastics, and machinery, which together accounted for more than 38 percent of China-origin TEUs in July. Volumes remain, however, below the record level set in July 2024 (1.02 million TEUs) and structural headwinds persist: elevated tariffs, intensified customs enforcement, new rules targeting transshipments via Vietnam, and the repeal of de minimis privileges may continue to put pressure on China’s share of U.S. containerized trade.

Widespread Port Gains Reflect Demand Pressure

July’s import spike was broadly distributed across U.S. ports. The top 10 ports saw a combined 20.4 percent month-over-month increase, led by Miami (35.5 percent), Houston (34.2 percent), and Oakland (31.3 percent). Even the largest gateways, Los Angeles (18 percent) and Long Beach (24.1 percent), posted strong double-digit gains.

Interestingly, East and Gulf coasts ports showed some of the sharpest rebounds in China-origin imports. Houston’s volumes from China climbed more than 120 percent, while Savannah, New York/Newark, and Charleston also recorded significant gains. In addition to seasonal demand, volume increases at the top U.S. ports reflect frontloading ahead of potential tariff policy changes and reinforce the strength of U.S. maritime imports.

Despite elevated volumes in July, port transit time delays rose only modestly during the month. New York/New Jersey delays increased by just 0.6 days, and Long Beach by 0.8 days, suggesting that U.S. port infrastructure is effectively managing the increased flow of goods.

Trade Diversification Continues

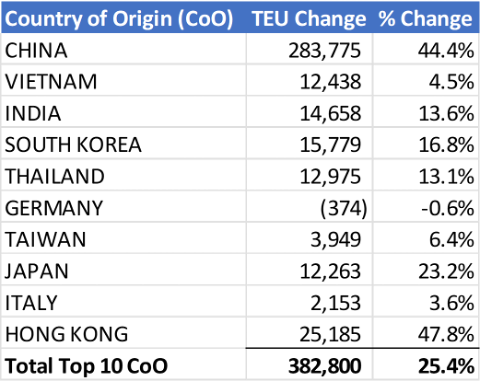

In addition to July’s month-over-month volume increase from China, U.S. imports from the top 10 countries of origin also shows a notable increase from Hong Kong (47.8 percent). Strong contributions also came from across Asia: South Korea (16.8 percent), India 13.6 percent), Thailand (13.1 percent), and Japan (23.3 percent), while Vietnam, Taiwan, and Italy posted more moderate gains. The widespread increases suggest a resurgence in Asia-origin shipments among U.S. importers.

Year-over-year, U.S. container imports from Southeast Asia continue to accelerate. Compared to July 2024, July 2025 volumes from India grew 24 percent, followed by Thailand (23.8 percent), and Vietnam (20.9 percent). While China clearly remains the dominant maritime trading partner for the U.S., other Asian countries are deepening their trade ties with U.S. importers amid ongoing diversification and shifting tariff policies.

Geopolitical Risks Add Complexity

While U.S. tariffs continue to dominate headlines, geopolitical disruptions remain an ongoing global logistics concern. Red Sea shipping routes continue to be heavily affected by Houthi attacks and Iran-Israel tensions, forcing carriers to reroute around the Cape of Good Hope. This has added up to two weeks of transit time and significantly raised insurance and freight costs. In addition to Red Sea volatility, Eastern European sanctions also continue to strain global trade routes.

Parting Thoughts

While the July surge in U.S. container imports is both a reflection of peak ocean shipping cycles and the impact of trade policy on global trade, it may represent a high-water mark rather than a sustained trend. For U.S. importers, however, it highlights the pressure of sustained uncertainty and the importance of building greater supply chain resiliency amid ongoing tariff turbulence and geopolitical volatility.

Jackson Wood is director of industry strategy at Descartes, the on-demand, software-as-a-service solutions provider.

Tags: Descartes Systems Group